Insights – Catch up Super Contributions- Are you leaving tax deductions on the table.

Superannuation is a fantastic tax vehicle for building long term wealth – with an income tax rate of 15%, a capital gains tax rate of 10% (for assets held longer than 12 months), and for most Aussies once they retire their super will become tax-free.

Super is also an excellent tax planning tool allowing us to claim a tax deduction for money that we contribute into our super, personally or by our employer on our behalf. These are called concessional contributions.

Its not all sunshine and rainbows though. Once your contribution (your money) enters the super system – that is where it stays, “locked away,” until you retire. So, depending on your age, income and cashflow – you will only want to contribute money that you can use to invest in the longer term.

Also, as with most things with the ATO, if there is a benefit, there are rules – lots of them and a cap which limits that amount you can benefit.

Concessional Contribution Rules

The rules relating to concessional contributions are dependent on your age and retirement status.

Any mandated superannuation guarantee (SG) contributions (most commonly contributions from your employer), are always acceptable. If you are working your employer must pay SG contributions no matter your age.

However, there are restrictions for voluntary contributions; salary sacrifice or personal contributions that you claim a deduction for in your own tax return.

- Under age 67 – No restrictions

- Aged 67 – 74 – must be working (minimum of 40 hours over 30 days)

- Aged over 75 – cannot voluntarily contribute to super

Concessional Contribution Cap

The cap (limit) on concessional contributions is $27,500 per year – no matter what you earn or how much you have in super.

Being an annual cap once the year passed its cap gone right?

Actually no – in some circumstances you can use any unused cap from prior years to contribute more to super in the current year and get more of a deduction.

Unused Concessional Cap Carried Forward Contributions

From 2019, those with less than $500,000 in total super, can contribute more than their annual concessional contributions cap by using any unused cap from the previous 5 years.

This is a rolling 5-year cap and any unused portion greater than 5 years will expire. Therefore 2023/24 is the last year we can unused any unused cap from 2018/2019 (noting the annual cap prior to 2021 was limited to $25,000)

Example:

| Description | 2018/19 | 2019/20 | 2020/21 | 2021/22 | 2022/23 |

| Annual cap | $25,000 | $25,000 | $25,000 | $27,500 | $27,500 |

| Employer Contributions | $13,000 | $11,000 | $nil | $8,000 | $27,500 |

| Unused annual cap | $17,000 | $14,000 | $25,000 | $19,500 | $nil |

| Total unused cap | $17,000 | $31,000 | $56,000 | $75,500 | $75,500 |

In this example in 2023/24 we could contribute an additional $75,500 on top of the $27,500 annual 2023/24 cap, provided that the total super balance was under $500k at the beginning of 202f financial year.

Strategic Opportunities

The Unused Carried Forward rule creates some unique tax planning opportunities:

Lumpy Income or time out of the workforce

Annual caps make it difficult for if you have lumpy income (where you have a cyclical businesses) or who have taken time away from work (raising children or caring for other family) to build your retirement savings.

Carry-forward contributions can help you catch up your super when you have more disposable income (paid off the mortgage or no childcare fees) and/or are back in the workforce.

Capital Gain

Where you have made a large capital gain from the sale of an investment property, shares or crypto, normally this gain would be added to your other income and taxed at your marginal rate; up to 47%.

However, you could use your unused carried forward cap and contribute into super (potentially from the sale proceeds) and use the tax deduction to help offset or eliminate the additional tax on the gain.

Inheritance or large windfall

You have received a large cash windfall; you can use your unused carried forward cap contributions to reduce your tax payable from your employment or other investments whilst moving the cash into a tax efficient investment structure.

Business Booming

Your business is booming however the company tax bill is growing and you’re accumulating too much cash (a great problem to have).

Your business could pay you additional salary sacrifice contributions above your normal annual cap using any unused carried forward cap. This provides the business with a tax deduction whilst building your retirement savings.

Super investment opportunity

You and your partner have your own business and need to move into a new commercial space.

You have the cash in the business, however buying the property in the business’s name creates some legal liability risks but getting the money out of the business creates a large tax issue.

By utilizing your unused carried forward cap you could withdraw the monies from the business, use the deduction to offset the additional tax and purchase the commercial space in an SMSF.

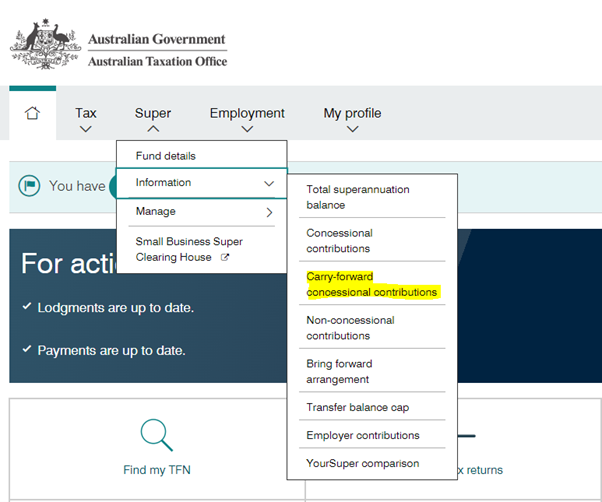

How to check the carry-forward amount available to you

You can access your unused carry-forward amount via myGov. Log in to myGov and select the linked ATO service.

Select the super tab >information > carry-forward concessional contributions

This will display your unused concessional contributions available to carry forward and confirm whether you are eligible based on your Total Super Balance which is calculated from information lodged with the ATO. If you have outstanding lodgements the information may not be up to date.

Alternatively, you can contact the ATO on 13 10 20 or speak with your accountant who should be able to access this information on your behalf.

Summary

Unused Concessional Cap Carried Forward Contributions can be a powerful tax planning tool to reduce your tax bill, catch up on your super and provide the opportunity for long term wealth accumulation.

However, with all thing’s superannuation getting the right advice at the right time is crucial. Always contact your accountant before your move any money around and consult with your financial planner to ensure that super contributions are in line with your overall financial plan.

How Can Alto Help?

Alto can help you to understand your eligibility to contribute and find out how much remaining caps you have, as well as deal with your every day super fund compliance matters. If you would like to know more about this strategy please don’t hesitate to contact our office.